Executive summary

Borrowers understandably obsess over loan economics, rate, LTC/LTV, proceeds, and “how much flexibility can I buy” at closing. But in real downside scenarios, the economics often become secondary to a harsher reality: the guarantor and covenant package is the true risk transfer mechanism. In other words, “non-recourse” frequently means “non-recourse until the loan documents say it isn’t.” [1]

Two underappreciated facts drive the point home. First, even “standard” agency-style documentation can include loss-based carveouts (misapplication of rents, failure to maintain insurance, waste, reporting failures) and full-recourse springing events (SPE/separateness failures, unpermitted transfers, bankruptcy events, certain fraud/misrepresentation categories). [2] Second, many guaranties are drafted as absolute and continuing obligations with broad waivers, designed to remain enforceable across assignments, foreclosure events, and a wide range of lender actions or inactions. [3]

The practical takeaway is contrarian but simple: a sponsor is often better insulated by negotiating guaranty scope, triggers, and burn-offs than by squeezing for more proceeds or a few basis points. That includes: (i) burn-offs tied to objective milestones (C/O, stabilization, DSCR/occupancy), (ii) caps and “loss-only” framing where possible, (iii) tighter definitions and cure rights to prevent technical-trips, and (iv) removing or neutralizing ambiguous clauses that create “discretionary default.” [4]

In that framework, credit enhancement, done carefully, can be a tool not just to “get approved,” but to reshape exposure (who signs, what burns off, what is capped, and when). CastleSquare operates in this co-guarantor/credit enhancement lane, providing net worth and liquidity support on qualified transactions where sponsors have strong deals but insufficient guarantor strength to satisfy lender requirements. [5]

Why borrowers overweight proceeds and pricing

I don’t blame borrowers for anchoring on proceeds. Most term sheets are designed to make the economic terms legible: coupon, fees, DSCR, LTC/LTV, reserves, covenants. Meanwhile, the guaranty package is often summarized in a sentence, until counsel starts marking documents, when time pressure is at its peak. The result is predictable: economics get negotiated; recourse gets “accepted.” [6]

There’s also a cognitive mismatch: proceeds and pricing are certain at closing, while guaranty liability is contingent. Contingent risks feel remote, until they’re not. Yet the formal documents themselves make clear that personal liability can be triggered by operational missteps, reporting failures, transfer technicalities, and bankruptcy-related events, not just “bad behavior” in the colloquial sense. [2]

Finally, lenders price loans to expected loss and capital, but they draft loan documents to protect worst-case outcomes. Many standard forms emphasize that lender remedies are cumulative and may be exercised without needing to show actual impairment, an important clue to how the document set is meant to function in stress. [7]

The covenant and guaranty surface area borrowers underestimate

The easiest way to see exposure is to map guarantees and covenants by what they protect, how they trigger, and how negotiable they are.

Agency small-loan programs provide a clean benchmark for financial covenants. For example, Fannie Mae[8] Small Mortgage Loans require combined borrower/key principal net worth at least equal to the original principal amount, and post-closing liquid assets equal to at least nine monthly payments of principal and interest. [9] Similarly, Freddie Mac[10] Optigo Small Balance loans require guarantor net worth equal to the SBL mortgage amount and liquidity equal to nine months of amortizing debt service (with additional requirements in certain cases, like entity guarantors). [11]

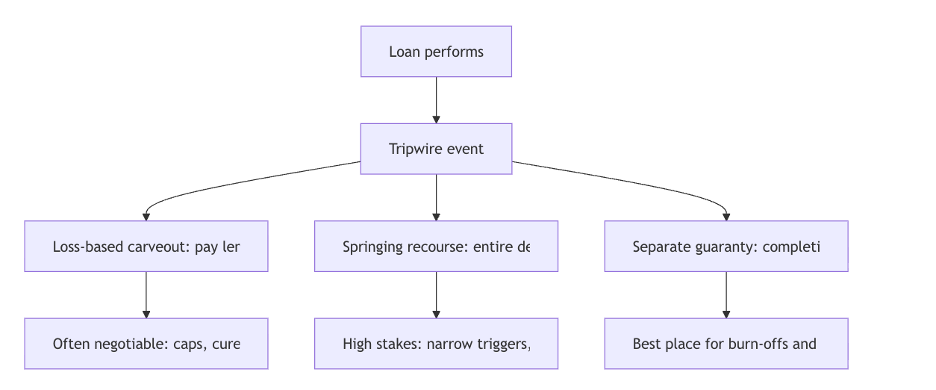

For non-recourse carveouts, the “standard list” is not static. One widely cited caution from Arnold & Porter, is that carveouts have grown in number and scope, and typically split into partial recourse (actual loss) and full recourse (springing) events, bankruptcy, transfer violations, and separateness/SPE covenant breaches being classic full-recourse triggers. [12]

The agency-style “personal liability” architecture illustrates this split concretely. A Fannie Mae-form non-recourse loan agreement can impose loss-based recourse for failures such as misapplication of rents and security deposits, failure to maintain required insurance, failure to apply insurance/condemnation proceeds properly, failure to deliver required reporting, waste/abandonment, and certain misrepresentations in ongoing reporting. [13] It can also spring to full recourse upon failure to comply with single-asset entity requirements, unpermitted transfers, and bankruptcy events (subject to nuance for involuntary filings), plus certain fraud/misrepresentation categories. [14]

Environmental exposure is its own category because (a) environmental law can impose strict and joint-and-several cleanup liability, and (b) loan documents often require independent contractual indemnities that can survive repayment and allocate costs broadly. U.S. Environmental Protection Agency[15] describes Superfund liability as retroactive, strict, and (often) joint and several. [16] A Fannie Mae environmental indemnity form example shows extensive notice obligations, survival language, and lender discretion in approvals. [17]

LIHTC transactions add a parallel universe of “return protection” mechanics. PNC Bank[18] (as an example of a large LIHTC equity participant) describes guarantees that commonly include construction completion, tax credit adjuster, operating deficit, recapture, and repurchase guarantees (with duration/amount determined by diligence and generally consistent with market). [19] On the public-policy side, Internal Revenue Service[20] guidance for housing joint ventures highlights the importance of limiting operating deficit guarantees by duration (e.g., not more than five years from break-even) and/or by scope (e.g., six months of operating expenses), and it discusses how tax credit shortfall/adjuster payments may need caps tied to developer fees. [21] Office of the Comptroller of the Currency[22] similarly notes that investors can use third-party guarantors for yield shortfalls and negotiate tax credit adjusters to reduce equity contributions when benchmarks affecting credits aren’t met. [23]

Covenant and guaranty comparison table

Lender incentives in distress and the “power” problem

A lender’s upside is capped (interest and fees). A lender’s downside is not (workout costs, time, reputational and regulatory friction, opportunity cost). So lenders build a second repayment path: guarantor liability and event-driven control rights. The documents often say this out loud, e.g., lender remedies are cumulative, can be exercised in any order, and may not require showing actual impairment or increased risk. [27]

In distress, the playbook tends to shift from “underwrite cash flow” to “enforce documents.” The Wells Fargo–Cherryland litigation is a warning shot that still matters: the Michigan Court of Appeals[28] enforced full recourse based on the borrower’s insolvency as a breach of SPE/separateness covenants, triggering full recourse under the documents, rejecting policy-based arguments and emphasizing that courts won’t save parties from bargains they didn’t fully understand. [29]

That’s why ambiguity is dangerous. When definitions rely on subjective lender discretion or loose “materiality” language, stressed lenders (or servicers) can weaponize technical breaches to create leverage. Negotiation sources aimed at borrowers consistently advise tightening the list of carveouts, distinguishing loss-only from full-recourse items, and demanding notice/cure rights for events that could trigger catastrophic liability. [30]

Tactical borrower strategies to limit exposure

This is the core: you don’t eliminate risk; you engineer it.

Start with the architecture. Many forms already distinguish (i) “loss-based” liability and (ii) “full recourse” liability. Borrowers should push that distinction harder: keep as much as possible in loss-based buckets, reserve “full recourse” for truly intentional misconduct (e.g., voluntary bankruptcy filings, intentional fraud). [31]

Second: burn-offs and burn-downs. Market commentary and practice guides recognize burn-off guaranties tied to performance incentives and benchmarks, and they explicitly identify “when does the guarantor get released?” as the central negotiation fight in carry guaranties (including post-transfer “tail”). [32]

Third: objective triggers and timing protections. Borrowers want defaults and guaranty triggers to be measurable (DSCR thresholds, occupancy tests, specific reporting dates) and to include notice/cure where feasible, because full-recourse exposure is “financial catastrophe” territory. [33]

Fourth: define covenants like a litigator. In many loan forms, “knowledge” can mean “after reasonable and diligent inquiry,” and lender approvals may be in the lender’s sole and absolute discretion, two phrases that behave badly in litigation. Tightening these standards, or at least cabining where they appear, reduces “gotcha” risk. [34]

Mermaid diagram: a burn-off timeline that actually reduces risk

This structure reflects what many lenders already underwrite to, completion, lease-up, and a financial performance test, while forcing the negotiation onto objective milestones rather than ongoing open-ended exposure. [35]

Mermaid diagram: how guarantor liability actually “flows” in a default

The goal is not “avoid all guaranties.” The goal is keep most outcomes in Z1, limit Z2 to provable bad acts, and time-limit Z3. [36]

Practical “What to Ask Before You Sign” checklist

1. Which guaranties exist, and which are loss-based vs full recourse? [37]

2. What exact events trigger springing recourse (bankruptcy, SPE, transfer, solvency concepts)? [38]

3. Where does the lender have sole/absolute discretion, and can we make triggers objective? [39]

4. What are the net worth/liquidity tests, how often tested, and what counts as “liquidity”? [40]

5. Are there cure rights for reporting, insurance, tax, and transfer technicalities? [41]

6. If this is construction/lease-up: what happens when the interest reserve runs out? Who funds it, and is there a “repack” risk? [42]

7. For carry guaranties: does liability end at deed-in-lieu/foreclosure, or is there a tail? [43]

8. For environmental: what survives repayment, what is “knowledge,” and what happens after a foreclosure event? [25]

9. For LIHTC: what adjusters/recapture obligations exist, how are they measured, and what are the caps? [26]

10. If the lender sells the loan or a special servicer steps in, do guaranty defenses get waived and do obligations survive assignments? [44]

Three hypothetical deal scenarios

A bridge loan where “9 months liquidity” is the real gating item: A sponsor wins a $45MM bridge loan on pricing and proceeds, then discovers the lender requires net worth equal to the loan amount and liquidity equal to nine months debt service, tested not just at closing, but with ongoing reporting. The sponsor has the real estate net worth but not the liquid balance sheet. Instead of over-contributing equity (and shrinking IRR), the sponsor negotiates (i) a defined liquidity schedule, (ii) a cure window to post eligible liquid assets, and (iii) replacement guarantor mechanics. This is the exact kind of covenant bottleneck that shows up in agency-style small loan guidance and in SBL underwriting standards. [45]

A construction loan where the “tail” becomes the hidden landmine: the project delivers late; the interest reserve is depleted. The bank requires additional cash to cover interest and operating costs, consistent with bank regulatory guidance noting that when reserves are depleted, banks generally require borrower or guarantor to add cash, while “repacking” reserves with additional debt can mask deterioration. The guarantor negotiates a carry guaranty burn-off at stabilization (DSCR test), and explicitly limits post-foreclosure tail to 60 days with a defined list of covered costs. [46]

A LIHTC deal where “economics” are fine but guarantees drive sponsor exposure: The sponsor focuses on equity pricing and construction financing. But the investor documents require construction completion, operating deficit, tax credit adjuster, recapture, and repurchase protections, i.e., the sponsor is guaranteeing credit delivery and yield stability, not just finishing the building. Public materials emphasize that investors use tax credit adjusters, and IRS guidance emphasizes limiting operating deficit guarantees by time and scope and capping tax credit shortfall payments tied to developer fees. [26]

Where credit enhancement fits and how CastleSquare shows up in practice

Credit enhancement is not a “get out of jail free” card. Done well, it’s a balance-sheet tool that can convert a binary outcome (“deal dies because sponsor doesn’t meet liquidity/net worth”) into a structured outcome (“deal closes with tighter, more documentable risk parameters”). That is why CastleSquare positions itself as a co-guarantor/credit enhancement partner providing net worth and liquidity to satisfy customary lender requirements, including for large loan sizes, and emphasizes speed and discretion. [47]

Subtly, the strategic value is not just “signing.” It’s creating negotiating room for: (i) burn-offs at objective milestones, (ii) caps for specific buckets (overrun, carry, certain indemnities), (iii) clearer triggers and cure rights, and (iv) tighter drafting that makes it harder to “trip” recourse when a lender is looking for leverage. Those are the same themes emphasized across borrower-focused guaranty negotiation guidance. [48]