Executive summary

Most CRE borrowers spend their time negotiating a term sheet, rate, proceeds, leverage, while treating the lender as interchangeable. That’s backwards. In bridge and construction lending especially, you are choosing a long‑dated counterparty with control over timing, cash, and remedies. Regulators have been explicit for decades that “loan administration” matters: documentation, disbursement, collateral inspection, collections, and loan review are core to safe real estate lending. [1]

The practical implication is simple: a lender can be “competitive” on paper and still create outsized borrower risk if it has (1) an enforcement-first culture, (2) a history of borrower-facing litigation rather than workouts, (3) friction or bottlenecks in draw funding, (4) fragile capitalization or liquidity, or (5) a funding model that can force abrupt behavior changes during volatility. [2]

This article lays out a high-level framework, built from primary regulatory guidance, public financial disclosures, and court records, to help sponsors evaluate a lender before starting the relationship. It includes two humanized, non-confidential examples from reputable trade press and court reporting, a short checklist, and a lender-selection decision flow that CRE executives can use across U.S. markets. [3]

The silent partner you didn’t mean to hire

At closing, a lender feels like a vendor. In the middle of execution, especially with construction holdbacks, it can feel like a partner. In a downside scenario, it can feel like a controlling stakeholder.

That transformation is not emotional; it is contractual and operational. Under long-standing banking standards, real estate lenders are expected to establish loan administration procedures that include disbursement and collateral inspection. [1] In other words, the industry’s “normal” is a model where the lender has both the right and the obligation to control the flow of funds and monitor progress. [4]

So the real question isn’t “Can they close?” It’s:

Who are they when the plan is late, the budget is tight, and your next draw is mission-critical?

The reason to underwrite the lender is not paranoia. It’s prudence. Federal regulators explicitly recognize that prudent CRE loan accommodations and workouts are often in the best interest of both the institution and the borrower. and they expect a balanced approach to evaluating workout practices. [5] That tells you something important: in the supervised banking world, “working constructively” is not supposed to be an exception; it is part of a sound credit culture. [6]

But not every lender, especially outside regulated banking, operates under the same incentives, liabilities, or scrutiny. [7]

Litigation history and reputation are behavioral credit metrics

Lawsuits are a visible proxy for how a lender behaves under stress

Workouts often happen in private. Litigation leaves footprints.

At the federal level, PACER[8] (Public Access to Court Electronic Records) provides public access to federal court records and notes it includes over a billion filed documents. [9] The system is also explicit about pricing mechanics, fees per page with caps, and waivers if usage stays under a quarterly threshold, meaning borrower diligence is practical if done efficiently. [10]

To complement PACER, CourtListener[11] hosts the RECAP Archive, an open, searchable repository of millions of PACER documents and dockets contributed through the RECAP system. [12]

What to look for (conceptually, not mechanically):

- Borrower-facing frequency: patterns of guaranty enforcement, foreclosure actions, or lender-liability disputes relative to the lender’s activity level.

- Posture: whether disputes read like “last resort enforcement” or “first resort leverage.”

- Consistency: whether the same issues show up repeatedly, funding cutoff claims, covenant traps, contested defaults.

No single docket proves character. But patterns across time, venues, and counterparties can reveal a lender’s operating philosophy. [13]

Reputation isn’t gossip; it’s market intelligence about incentives

The market’s “predatory” label often points to a particular fear: that a lender views the loan as a path to control, not a path to repayment.

In restructuring practice, “loan-to-own” is commonly described as an acquisition strategy where an investor or lender expects to convert a debt position into ownership of assets or equity through distress mechanics, sometimes by buying a controlling tranche of debt and using credit-bidding power in a sale process. [14] In CRE, the analog is straightforward: the lender’s remedies, and how quickly they are willing to use them, shape whether you have room to recover from a normal business-plan slip.

That’s why sophisticated sponsors should treat lender reputation as a due diligence category, not a vibe, and triangulate it across brokers, borrower-side counsel, and prior borrowers, especially those who had a “messy middle,” not just a clean exit. [15]

In bridge and construction loans, draw funding is the real product

When a loan includes holdbacks and a draw schedule, the “rate” is not what keeps the project alive. Cash velocity does.

Regulatory guidance for construction and land development lending highlights “disbursement controls,” including periodic inspections during construction, and lien waivers as standard risk controls. [4] The Office of the Comptroller of the Currency[16] goes a step further in its handbook: failure to properly monitor construction progress and manage the disbursement of proceeds is explicitly characterized as a control weakness that increases credit risk, and insufficient staffing or expertise increases operational risk. [17]

Borrowers should read that carefully. If a lender is understaffed, reliant on slow third parties, or inconsistent in inspections, the draw process becomes a hidden risk premium, paid in delays, contractor friction, re-trades, and lost time.

Humanized example: when funding friction becomes the dispute

In a widely reported dispute covered by The Real Deal, an entity tied to [Borrower] alleged that its lender, [Lender], stopped funding disbursements for the [Project] development in Newark and claimed the lender was undercapitalized; the lender disputed the allegations.

You don’t need to take a side in a pending dispute to learn the lesson: if the draw process breaks, everything downstream breaks, construction schedules, subcontractor confidence, insurance and tax timing, leasing momentum, and ultimately the borrower’s negotiating position. And when capital health is questioned at the same time as funding performance, the borrower is exposed to two risks at once: operational delay and counterparty fragility.

Capitalization, funding model, and the hidden partner problem

“Well-capitalized” is not a marketing adjective; it’s a balance-sheet question

Before you borrow, you should understand how your lender funds itself and how much flexibility it has when markets tighten.

If the lender is public, SEC filings are the most direct window. The U.S. Securities and Exchange Commission[23] explains that annual reports on Form 10‑K provide a detailed picture of a company’s business, risks, and financial results, and follow a standardized structure. [24]

If the lender is a bank, you have unusually strong transparency. The FFIEC[25] provides public access to Call Reports and the Uniform Bank Performance Report (UBPR) for most insured institutions, and describes UBPR as an analytical tool that helps evaluate earnings, liquidity, capital, and balance-sheet composition. [26]

The conceptual point: you want to know whether your lender has the liquidity and resilience to be patient.

The Federal Deposit Insurance Corporation[27] defines liquidity as the ability to meet cash and collateral obligations at a reasonable cost and cautions that failure to manage liquidity risk can quickly result in negative consequences, including failure. [28] If that’s true for banks with regulators watching, it’s even more relevant when evaluating nonbanks where market funding can change quickly.

The funding model shapes lender behavior under stress

Lenders are not all built the same:

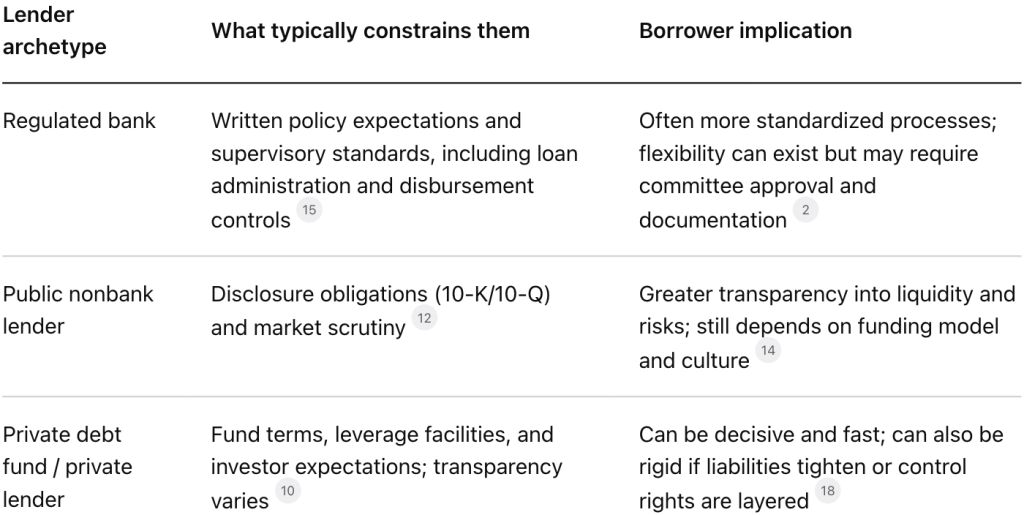

- A balance-sheet bank lender tends to be constrained by policy, process, and supervision. [29]

- A fund lender may be constrained by fund terms, subscription lines, leverage facilities, and investor redemption or concentration dynamics. [30]

- A lender reliant on warehouse lines or repurchase agreements may face short-term funding pressures that translate into fast shifts in posture. [31]

On warehouse and repo mechanics, Mortgage Bankers Association[32] describes two common structures: warehouse lines of credit and Master Repurchase Agreements (MRAs), often called “repo.” [33] While the MBA discussion is focused on mortgage banking, the broader idea generalizes: short-term, collateralized financing frameworks can transmit market stress into operational behavior. [34]

The Financial Stability Board[35] notes that when volatility spikes, cash borrowers may need additional liquidity to meet margin calls and cash lenders may be unable or unwilling to provide funding in stress periods. [34] That is a systemic observation, but it should sharpen a borrower’s instinct: if your lender’s liabilities can reprice or tighten overnight, your loan administration experience can change overnight too.

A-note partners: the decision-maker may not be in the room

Many borrowers assume the “lender” has unilateral decision authority. In structured credit, that is often false.

In A/B note structures, third-party materials commonly describe the B-note holder as acting as a “Controlling Noteholder” or similar role, meaning the party with economic exposure may also have key workout or enforcement influence depending on the intercreditor framework. [36] Even older but widely cited structured-finance practice materials emphasize that relationships between noteholders are governed by intercreditor agreements that can allocate control in meaningful ways. [37]

For borrowers, the high-level diligence ask is not legalistic: it is practical.

Who must approve an extension, a budget change, a leasing decision, or a waiver when the plan is off by a quarter?

Default philosophy and technical defaults are the lender’s “values statement”

Every lender says it is relationship-oriented, until the relationship is tested.

Regulators explicitly encourage a constructive posture toward creditworthy borrowers under stress. In the interagency CRE workout policy statement, the agencies state that many borrowers will remain creditworthy and that institutions may find it beneficial to work constructively with borrowers through accommodations or workouts; the statement also says prudent accommodations and workouts are often in the best interest of both the institution and the borrower. [6]

That is what “good” looks like in the regulated standard.

But borrowers must evaluate whether a lender’s incentives align with that posture. Some lenders view time and flexibility as tools to preserve value. Others view time as an enemy and default as an opportunity to gain leverage.

This is where technical defaults matter. A lender that routinely weaponizes minor covenant issues, reporting timing, budget re-approvals, cash-management triggers, can create a dynamic where the borrower is negotiating from a permanent state of vulnerability.

Humanized example: the power of waivers and “absolute” guaranties

A recent Reuters report on a Southern District of New York decision illustrates a common borrower blind spot: the enforcement power embedded in guaranty language. In that case, the court enforced an “absolute and unconditional” guaranty and rejected guarantor defenses and counterclaims that were broadly waived, reinforcing how tightly drafted guaranties can narrow a guarantor’s ability to litigate lender conduct after default. [38]

Again, the lesson is not “never sign a guaranty.” It’s that lender selection should include a candid assessment of how aggressively a lender documents, declares, and enforces defaults, and how much discretion it reserves. [39]

“Loan-to-own” and fast remedies are not theory in CRE

In mezzanine contexts, the Uniform Commercial Code provides a framework where, after default, a secured party may dispose of collateral (subject to commercial reasonableness and notice rules). [40] Courts regularly adjudicate whether a UCC sale process was commercially reasonable, demonstrating that these remedies are real and litigated. [41]

If your capital stack includes fast-remedy instruments, lender behavior and lender incentives become even more central to outcomes.

How to Underwrite Your Lender

The goal is conceptual: identify counterparty risk before it becomes execution risk.

Practical checklist

- Behavior under stress: Look for public signals (court records) and private signals (market reputation) that indicate “workout-first” vs. “enforcement-first.” [42]

- Litigation footprint: Use PACER and CourtListener to understand the lender’s borrower-facing litigation patterns and language themes over time. [43]

- Draw credibility: For bridge/construction, ask whether the lender’s operational setup can reliably execute disbursements, inspections, and lien controls, regulators treat these as core risk controls. [44]

- Balance-sheet reality: If the lender is a bank, use UBPR/Call Reports; if public, use 10‑K/10‑Q; if private, be wary of opacity and lean more heavily on references and structure protections. [45]

- Funding model fragility: Understand whether the lender relies on warehouse/repo-style funding structures that can transmit volatility through margin and liquidity demands. [46]

- Hidden decision-makers: Identify any A-note partner and who has consent rights in the downside; structured deals can allocate control away from the front-facing relationship manager. [47]

- Technical-default temperament: Evaluate how the lender documents defaults and guaranties; court outcomes show that waivers and “absolute” guaranties can significantly constrain defenses. [38]

Tables

Lender archetypes: what usually drives their behavior

Evidence availability: where borrowers can actually verify strength and behavior | Attribute you care about | Banks | Public nonbanks | Private lenders/funds | |—|—|—| | Financial strength (capital/liquidity) | High: Call Reports + UBPR [26] | High: 10‑K/10‑Q [49] | Mixed: depends on disclosure; often reference-driven [28] | | Draw process discipline | Medium: policies exist; execution varies [44] | Medium: execution varies; staffing matters [17] | Medium: depends on operational build-out; diligence is critical [4] | | Litigation footprint | Medium-high: public dockets still accessible [13] | Medium-high: public dockets still accessible [9] | Medium-high: still visible in court records [51] | | Workout philosophy | Medium: regulators explicitly support prudent workouts [6] | Medium: depends on internal culture and incentives [28] | Medium: depends on strategy and downside underwriting [52]

CastleSquare positioning

CastleSquare’s role in the market is best understood as credit enhancement for CRE sponsors: helping borrowers present stronger credit stories, choose safer counterparties, and negotiate financing that reduce avoidable failure points, especially where draw mechanics, layered control rights, or liquidity-sensitive funding models can turn a normal variance from plan into an existential problem.