Executive summary

Agency multifamily execution in 2026 is less about “checking boxes” and more about whether your deal reads as institutional, enforceable, and monitorable from Day 1 through maturity. The core pattern across both agencies is consistent: clean ownership, credible guarantor optics, and underwriting that survives scrutiny under stress. [1]

Three practical realities dominate approvals and investor comfort:

- Ownership requirements are underwriting. Both agencies hardwire “who owns what, and can control change” into eligibility and fraud controls, down to domestic-entity rules, SPE/single-asset constraints, and transfer mechanics. [2]

- Guarantor optics are now a first-order risk factor. In 2024–2026 guidance, “who backs the deal” is inseparable from enhanced due diligence (First-Time / Limited Experience / Rapid Growth), liquidity validation, and even how lenders document adverse findings. [3]

- Underwriting nuance is where deals win or die. Stress discipline (rates, capex, exit), documentation chain-of-custody, and narrative coherence are explicitly emphasized, especially for refis and sponsors with non-standard profiles. [4]

Where CastleSquare’s Credit Enhancement Program fits: it can strengthen eligibility and investor comfort when the “gap” is balance-sheet strength or guarantor credibility, but it does not cure structural ineligibility (e.g., non-U.S. borrower entity where prohibited; missing sponsor control where required; messy title/closing chain). [5]

Ownership and sponsor experience requirements

Ownership structures the agencies can underwrite in 2026

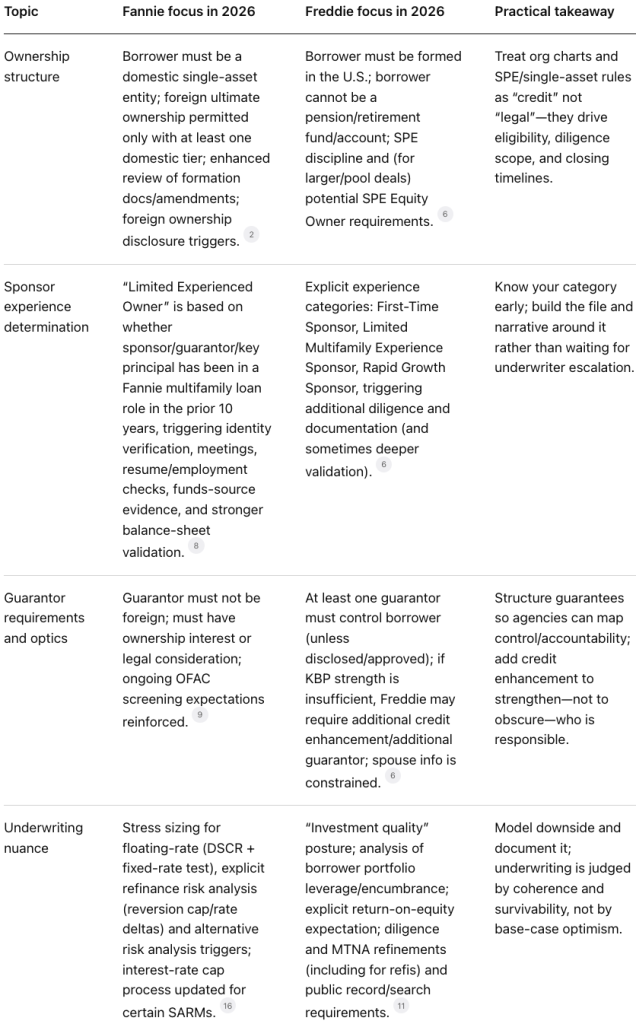

Fannie: domestic single-asset logic with explicit foreign-tier and mezzanine constraints. The Multifamily Guide requires the borrower to be a domestic single-asset entity formed solely to own the property, and if the borrower is ultimately foreign-owned, it must include at least one domestic tier of ownership. [6]

If the borrower owns more than one asset, Fannie’s guidance does not simply “allow it”; it conditions “single-asset” status on evidence such as no existing debt liens on other real property, no mezzanine financing on equity interests, and loan document prohibitions on acquiring additional debt/real property (with limited exceptions). [6]

Freddie: U.S.-formed borrower + SPE discipline + control-aware guardrails. Freddie’s Guide states the borrower must be an entity formed in the United States, and it frames borrower eligibility around defined entity types while expressly barring certain borrower profiles (e.g., borrower cannot be a pension/retirement fund/account). [7]

Freddie also requires SPE features broadly: property must be the borrower’s sole asset and operating it must be the borrower’s sole business, with additional SPE mechanics for larger loans and pooled/cross-collateralized situations (including the potential need for an SPE Equity Owner at certain loan sizes/structures). [7]

What “ownership clarity” means in practice

In 2025, Fannie updated its loan documents to add/refresh concepts lenders have to operationalize: new/updated definitions (including domestic/foreign person concepts, organizational chart requirements, and blocked-person framing) and new Transfer restriction language addressing principals, preferred equity/mezzanine financing, and “new borrower/guarantor/key principal/principal” scenarios. [8]

This aligns with a broader fraud-prevention posture that requires lenders to document due diligence findings in the Transaction Approval Memo and to deepen formation/ownership review. [9]

How sponsor experience is determined, and where the agencies differ

The agencies do not treat “experience” as a vibes-based discussion in 2026, they encode it into categories, triggers, and documentation.

Fannie’s key trigger is “Limited Experienced Owner,” which is Fannie-history based. Fannie defines a Limited Experienced Owner as a person who has not been a sponsor/key principal/guarantor for a Fannie multifamily loan in the prior 10 years, and then mandates enhanced identity, meeting, resume, employment verification, funds-source, and balance-sheet validation steps. [10]

Notably, those steps include: in-person/virtual meetings with individuals behind key roles and controlling interests, resumes, employment verification via tools like LexisNexis[11] (or similar), and best-efforts real estate valuation verification (e.g., via CoStar[12] or similar). [13]

Freddie’s framework is deal-role and property-control based, and it is explicitly graded. Freddie defines:

– First-Time Sponsor: neither the Key Borrower Principal nor its ultimate control has transacted with Freddie in a similar role in the past 10 years. [7]

– Limited Multifamily Experience Sponsor: neither the Key Borrower Principal nor its ultimate control has controlled at least five substantially similar properties within the past five years. [7]

– Rapid Growth Sponsor: control of 15+ multifamily properties with 50%+ acquired in the past three years (effective for transactions after Feb. 27, 2025, subject to supporting documentation if ultimate control differs). [14]

Freddie then links these categories to “additional due diligence requirements” and underwriting checklist expectations. [15]

Guarantor optics and credit support

The “guarantor problem” in 2026 is more than net worth

Investor and agency scrutiny increasingly distinguishes between: (a) a guarantor who is merely “rich,” and (b) a guarantor who is understandable, tied to governance, and diligence-able. That shows up in formal policy changes.

Fannie’s guardrails: foreign guarantor prohibition + AML/OFAC expectations. Fannie’s Guide requires the guarantor to not be a foreign person or foreign entity and to have either an ownership interest in the borrower or sufficient legal consideration to enter the guaranty. [16]

Fannie also hardens ongoing compliance expectations: maintaining effective OFAC compliance procedures, including monthly screening of borrowers, guarantors, key principals, and principals, and rapid reporting of blocked/sanctioned persons. [17]

Freddie’s guardrails: control + capacity + documented diligence. Freddie requires that if there is a guarantor, at least one guarantor must have control of the borrower unless previously disclosed and approved. [7]

Separately, Freddie’s underwriting language makes clear that if a Key Borrower Principal’s financial strength is insufficient, Freddie may require additional credit enhancement or an additional guarantor. [18]

2024–2026 policy changes that directly reshape guarantor optics

Freddie made multiple due diligence expansions that change how guarantors and sponsor principals are “seen”:

- April 18, 2024: additional Key Borrower Principal due diligence, bank/brokerage statements to validate liquidity and verified real estate schedule ownership; plus MTNA requirements to flag whether the sponsor is First-Time / Limited Experience. [19]

- August 15, 2024: standardized public records searches (bankruptcy, tax lien, litigation; criminal; web searches), fresh-dated within 60 days, with summaries of adverse findings required in the MTNA (or acceptable substitute). [20]

- February 27, 2025: enhanced due diligence for Rapid Growth Sponsors and sampling-based verification of assets on Form 1116. [21]

- August 26, 2025: Freddie underwriting expanded mark-to-market net worth validation (effective Aug. 26, 2025: applies to all Key Borrower Principals) and required broader asset reflection on Form 1116; also expanded acquisition closing funds analysis to all acquisitions. [22]

- December 16, 2025: Freddie reinforced enhanced due diligence and revised refinance narrative analysis requirements (and clarified SBL guarantor items). [23]

Fannie’s 2025 fraud prevention update and related communications also raise the “optics floor” by requiring documented due diligence findings, deeper ownership review, property internet searches, and tighter ACheck timing for certain profiles. [24]

Underwriting nuance and documentation that drives approvals and pricing

Underwriting is now explicitly “stress-first”

Fannie’s guidance for floating-rate/ARM underwriting makes the theme explicit: size to the lowest amount under DSCR at stressed rates and the fixed-rate test, and use the fixed-rate test rate for refinance risk analysis. [25]

Fannie’s refinance risk analysis guidance also pushes lenders to widen the gap between entry and exit assumptions (e.g., higher reversion cap and refinance rate) and to provide alternative risk analysis when base assumptions don’t fit reality or when third-party data suggests weaker rent growth than published growth rates. [26]

Freddie’s underwriting chapter lays out both objective and subjective factors and ties them to “investment quality,” including explicit attention to borrower holdings being over-encumbered and to whether the borrower/principals can meet loan obligations across a portfolio. [27]

Freddie also states it will not purchase a mortgage unless there is a positive return on the borrower’s equity (before income taxes). [18]

Documentation chain-of-custody is part of risk control, not “ops”

Freddie’s 2025 bulletin added delivery requirements that read like anti-fraud controls: chain of title during the prior 36 months, closing statements/escrow instructions, and receipts/disbursements ledgers with wire/check evidence (effective for certain loans on/after Oct. 1, 2025). [22]

Freddie also increased rigor around public records searching and required summarization of adverse findings in the MTNA. [20]

Fannie’s 2025 fraud-prevention update similarly requires documentation of due diligence findings in the Transaction Approval Memo and added requirements for site inspections/lease audit style controls, plus property internet searches and management oversight items. [9]

Interest-rate hedge administration is now a servicing-and-eligibility lever

Fannie’s December 10, 2025 Supplement revised delegated authority around structured ARM (SARM) interest rate caps, allowing delegated approval of shorter-term caps in defined cases and requiring recalculation of cap escrow payments at least every six months for delegated use. [28]

This matters for lender/sponsor credibility because hedge administration is increasingly viewed as a forward-looking execution risk (especially when cap pricing and liquidity are volatile). [29]

CastleSquare Credit Enhancement Program and agency outcomes

CastleSquare’s Credit Enhancement Program is positioned as a balance-sheet and guarantor-capability solution: CastleSquare can provide net worth and liquidity as a co-guarantor to meet customary lender requirements, able to post up to “9-figures of liquidity” and “10-figures of net worth,” and a process that includes underwriting and stress testing. [30]

How it interacts with agency criteria in 2026

Where it can help agency execution (typical “yes” use cases):

- Net worth / liquidity shortfalls: If the sponsor/operator and deal are otherwise agency-sound, adding a credible co-guarantor can improve the “can this borrower support the property in downside scenarios?” thesis, especially where Freddie contemplates “additional credit enhancement” when Key Borrower Principal strength is insufficient. [31]

- Speed-to-close pressures: The program markets fast turnaround and discretionary support, which is relevant when agencies’ documentation expectations (public records, ownership charts, chain-of-custody, etc.) create timing risk late in the process. [33]

Where it cannot fix agency ineligibility (typical “no” use cases):

- Entity / control non-compliance: Freddie’s rule that at least one guarantor must have control (unless disclosed/approved) means a non-controlling third-party guarantor is not a plug-and-play replacement for sponsor control. [7]

- Foreign-guarantor constraints at Fannie: Fannie requires the guarantor not be a foreign person/entity; CastleSquare may still work (if domestic), but it cannot override the rule. [16]

- Document-chain and title problems: Enhanced closing documentation and chain-of-title expectations are separate from guarantor support; a credit enhancer can’t cure unclear flow of funds or missing title-chain evidence. [22]

Practical playbook with vignettes, best practices, risks, and FAQ

Comparison table

Case vignettes

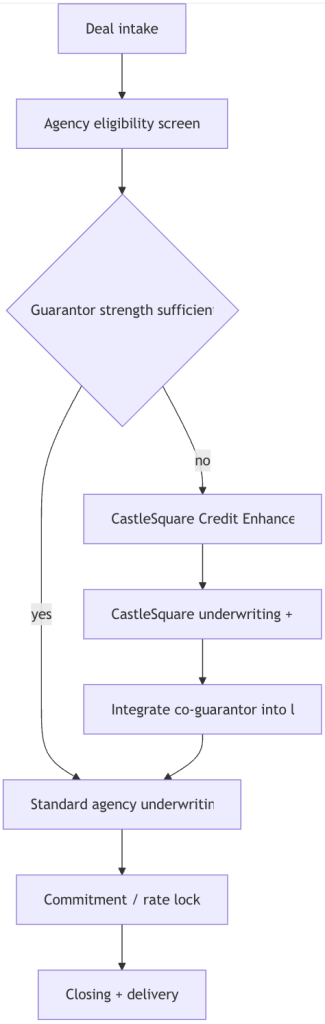

Vignette: Compliance (ownership + experience + credit support)

A sponsor pursuing a $65MM acquisition sets up a borrower that is cleanly SPE/single-purpose, provides a full org chart down to all relevant owners, and runs required screening early (including ACheck timing where applicable). A minority foreign LP is disclosed with a domestic-tier structure (where allowed), and the lender documents diligence findings in the narrative memo. Facing a liquidity shortfall for guarantor standards, the sponsor brings in CastleSquare as a co-guarantor early enough to integrate into underwriting, governance, and document flow. [41]

Vignette: Pitfall (guarantor optics + control mismatch)

A borrower attempts to “solve” Freddie guarantor requirements by inserting a non-controlling third-party guarantor late in the process while the controlling sponsor remains balance-sheet constrained. Freddie’s Guide framework emphasizes that at least one guarantor must have control (absent prior disclosure/approval), and underwriting may require additional credit enhancement in addition to (not instead of) control-aligned guarantors. The late change triggers expanded diligence, narrative rewrites, and timeline slippage. [42]

Vignette: Pitfall (documentation chain and fraud-prevention triggers)

A refinance file includes inconsistent sources-and-uses support and incomplete evidence of fund flows and title-chain transactions. Under 2024–2025 Freddie bulletin updates, delivery expectations can include chain-of-title documents, closing statements/escrow instruction letters, and receipts/disbursements ledgers with wire/check evidence; adverse public record findings must be summarized in the MTNA. Missing these elements becomes an approval drag regardless of DSCR/LTV. [43]

Best practices and tactical steps for 2026

1) Front-load ownership clarity (not just legal formation). Build a lender-ready org chart that makes it easy to identify principals and controlling interests, and keep it version-controlled through closing. [44]

2) Treat sponsor experience as a category, not a narrative.

– For Fannie: determine whether any key party fits “Limited Experienced Owner” and complete the additional steps early (meetings, resumes, employment verification, origin-of-funds evidence, liquidity validation). [10]

– For Freddie: determine sponsor category (First-Time / Limited Experience / Rapid Growth) and build the package (bank/brokerage statements for liquidity, Form 1116-quality schedules, and proof of asset ownership where required). [45]

3) Document diligence in the right “narrative container.”

Fannie: Transaction Approval Memo documentation expectations were explicitly reinforced. [9]

Freddie: MTNA (and servicing PLIM where relevant) is repeatedly used as the required repository for disclosures and summaries of adverse findings. [46]

4) Underwrite exits like an investor, not a sponsor.

Adopt rate/cap stress that is defensible and align your refinance risk analysis and growth assumptions with “what could break.” [47]

5) Integrate credit enhancement early enough to be “underwritten,” not “patched.”

CastleSquare’s program offers co-guarantor support with its own underwriting/stress testing; that value diminishes if introduced after agency diligence and document flow are already in motion. [30]

Regulatory and market risks through 2026

FHFA multifamily caps and mission-driven composition will shape execution strategy. FHFA set 2026 multifamily loan purchase caps at $88B per enterprise and required at least 50% mission-driven, affordable housing, with workforce housing excluded from the caps (and continued monitoring/possible upward adjustment). [48]

Implication: lenders and sponsors should expect continued attention to product/mission fit and portfolio mix, this can affect pricing, pacing, and prioritization even when a deal is credit-sound. [49]

Policy volatility around the GSEs remains headline risk. Reporting in late 2025–early 2026 described renewed discussion of potential public offerings and government-directed MBS portfolio activity, which can influence investor sentiment and secondary-market expectations even when multifamily credit remains stable. [50]

Operational-risk regulation is effectively embedded in agency guides now. Expanded fraud-prevention steps, record searches, chain-of-custody documentation, and ongoing sanctions screening increase the cost of being “sloppy”, and can delay closings or create post-close enforcement risk. [51]

FAQ

Is a third-party credit enhancer enough to satisfy Freddie’s guarantor requirement?

Not automatically. Freddie’s Guide states that for any mortgage with a guarantor, at least one guarantor must have control of the borrower unless previously disclosed to and approved by Freddie Mac. [7]

Can a foreign individual/entity be the guarantor on a Fannie multifamily loan?

Fannie’s guidance states the guarantor must not be a foreign person or foreign entity (and also addresses foreign ownership disclosures). [16]

What triggers “enhanced due diligence” for sponsor/principal profiles in 2026?

Freddie triggers include First-Time Sponsor, Limited Multifamily Experience Sponsor, and Rapid Growth Sponsor categories. [14]

Fannie triggers include “Limited Experienced Owner” status and related fraud-prevention diligence expectations (plus ACheck timing and SREO collection updates). [52]

What underwriting behavior most often causes agency pushback in refis?

Expect pushback when exit assumptions are not credible (cap/rate reversion), when growth assumptions deviate without support, or when narrative analysis fails to align diligence findings to credit conclusions. [53]

Does credit enhancement replace sponsor experience?

No. Both agencies’ guidance shows experience is evaluated alongside credit strength, governance/control, and documented diligence. Credit enhancement can strengthen the “supportability” of the deal, but it does not substitute for control-aligned responsibility or for required diligence artifacts. [54]

CastleSquare’s Credit Enhancement Program

CastleSquare’s Credit Enhancement Program is a a co-guarantor solution designed to close the common gap between strong real estate fundamentals and borrower balance-sheet requirements: CastleSquare can provide net worth and liquidity support, able to post up to “9-figures of liquidity” and “10-figures of net worth”, and sign as a co-guarantor on fully underwritten, transaction-specific deals, with an emphasis on speed and confidentiality. Used correctly, it can improve agency eligibility and investor comfort when the missing piece is credible guarantor strength, while preserving the agency-driven need for clean ownership, control clarity, and robust diligence. [55]

Optimal time to bring CastleSquare into the Closing